Whether the result of a booming economy, tighter immigration laws or an educational system gone astray, finding qualified pond construction job applicants has become increasingly more difficult for those in this industry. Even more troubling for smaller businesses is the question of how they can compete for badly needed, qualified workers.

Surprisingly, survey after survey shows that it is not money alone that attracts new workers and keeps existing employees on the job — it’s the benefits. In fact, the flexibility and the opportunity to balance work with other life responsibilities, interests and issues are treasured by job seekers and employees alike.

Fortunately, thanks to our unique tax laws, every retailer, distributor, manufacturer and contractor can afford to offer fringe benefits to their workers — and may even be able to benefit themselves. That’s right; our tax laws only prevent employers from discriminating in favor of owners, key employees and other highly compensated individuals when setting up benefits plans that are both tax-deductible for the business and tax-free for the recipient.

Fringe Benefits

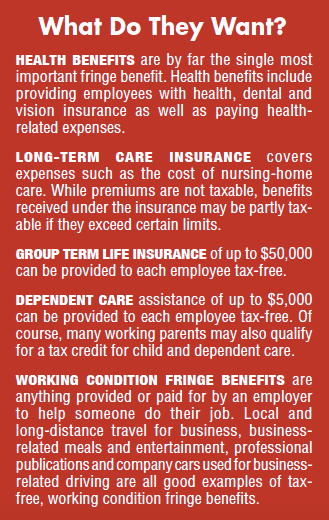

Fringe benefits are defined as property and services whose benefit to employees frequently outweighs the cost to the employer. With a number of notable exceptions, fringe benefits are generally included in an employee’s gross taxable income, where they are subject to income tax withholding and employment taxes.

These tax savings obviously make fringe benefits an attraction. However, thanks to the Tax Cuts and Jobs Act of 2017 (TCJA), the array of tax-free fringe benefits that employers can provide is not quite as generous as it used to be.

Retain & Train Your Workers

Surprisingly, survey after survey shows that it is not money alone that attracts new workers and keeps existing employees on the job — it’s the benefits. In fact, the flexibility and the opportunity to balance work with other life responsibilities, interests and issues are treasured by job seekers and employees alike. No garden pond professional can be an employer of choice without a good benefits package. Job training, educational assistance and employer-provided vehicles used for business are among the common working-condition fringe benefits provided by many small businesses.

On-the-job training provided by an employer is a tax-free hiring incentive and an invaluable perk for current employees. Educational assistance and tuition reimbursement are also welcome fringe benefits.

A formal, written educational assistance plan doesn’t necessarily mean immediate employer funding. Some effective plans provide reimbursement for an employee’s educational expenses — up to $5,250 per employee per year, exempt from tax. Educational assistance includes not only tuition, but also payments for books, equipment and other expenses related to continuing education.

Ways to Beat the Competition

While pay often isn’t the primary goal of many job seekers, every pond business owner and manager should keep in mind that in today’s job market, compensation remains an important factor. By surveying the local job market and the compensation offered by others in the pond industry, a retailer, distributor, manufacturer or builder can offer higher pay than average to attract the best candidates.

Benefits offered by a pond business should also be above industry standards, with new fringe benefits added when they are affordable. Existing employees should be educated about the cost of their benefits so they appreciate that their needs are being addressed.

Benefits offered by a pond business should also be above industry standards, with new fringe benefits added when they are affordable. Existing employees should be educated about the cost of their benefits so they appreciate that their needs are being addressed.

Job seekers and employees are increasingly looking for cafeteria-style benefit plans in which they can balance their choices with those of a working spouse or partner. Bonuses that pay employees for measurable achievements and profit-sharing plans can be invaluable.

Again, bonuses and awards must be included in an employee’s taxable income. Should the bonus or award be in the form of goods or services, employees must include the fair market value of those goods or services in their income. The same applies to holiday gifts. However, employees receiving turkeys, hams or similar items of nominal value from their employers at Christmas or other holidays may exclude the value of the gift from their income.

A profit-sharing plan, often called a “deferred profit-sharing plan” (DPSP), gives employees a share of the operation’s profits. Under this type of plan, an employee receives a percentage of the operation’s profits based on its quarterly or annual earnings, regardless of the size of the operation. This is a great incentive to attract new workers and a way to enable your employees to feel sense of ownership in the business. Not too surprisingly, however, there are restrictions on when and how a person can withdraw these funds without a penalty. The contribution limit for a pond business that shares its profits with an employee is the lesser of 25 percent of the employee’s compensation or $55,000. In order to implement a DPSP, the business must file I.R.S. Form 5500 and disclose all participants of the plan. Just as with other retirement plans, early withdrawals are subject to penalties.

An Employee Stock Ownership Plan (ESOP) is an employee-owner program that provides workers with a tax-free ownership interest in the pond business. An ESOP is a qualified, defined-contribution employee benefit plan designed to invest primarily in the stock of the employer. In general, employees are provided with ownership at no upfront cost. The shares provided can be held in a trust for safety and growth until the employee retires or resigns. At that time, the shares either go back to the business for further redistribution or are completely voided.

At the Very Least

So-called “de minimis” benefits may be worth little or nothing in the eyes of lawmakers, but they go a long way toward making employees — and prospective employees — happy without an accompanying tax bill. De minimis fringe benefits refer to any property or service that is so small in value that accounting for it is unreasonable or administratively impractical.

A happy workplace is always an attraction for job seekers. Whether it’s a nightclub affair or a buffet in the business’s break room, parties are a tried-and-true benefit. And, in addition to making employees feel valued and keeping them motivated, parties have tangible tax benefits. The tax rules allow a business to throw a holiday party — even a relatively fancy one — with no tax consequences to the employees.

Of course, in order to be deductible, the I.R.S. requires any cost to be “reasonable.” A garden pond professional cannot deduct expenses for entertainment that are considered lavish or extravagant.

It should also be of note that the TCJA included important changes to the tax treatment of employer-sponsored benefit programs. The new law restricts an employer’s ability to deduct many common business expenses, such as meals, entertainment and employee moving-expense reimbursements. On the upside, though, the law also included a new tax credit for employers who provide paid family and medical leave for employees.

[box]>> Related Content | Contractor Crackdown: The heavy cost of misclassified workers. [/box]

The bottom line is, in order to attract and retain talented individuals at your pond business, you must offer fringe benefits and other perks. Once you have determined what benefits will best attract the specific workers you need in today’s job environment, which benefits new and prospective employees would prefer, and which benefits the pond business can really afford, only then can you make an informed choice among them.

And, hey — wouldn’t it be ironic if the benefits you choose to offer and their associated additional expenses actually ended up saving your operation more money?

With 25 years of professional experience in taxes and finance, Mark Battersby writes on unique and topical subjects in the

industry.

Although no reputable professional should ever render specific advice at arm’s length, he does craft unbiased, interesting, informative and accurate articles.