Over the past 20 years, a lot has changed in our pond-building business. Some of those changes have made a fairly large impact on our business. One of these is how consumers pay for their pond installations. When we started our pond business in the mid ‘90s, I would meet a water feature customer at their site, design the pond of their dreams and then provide them with a quote. If the customer wanted to move forward with the project, I would collect a 50-percent deposit and schedule the job.

Over the past 20 years, a lot has changed in our pond-building business. Some of those changes have made a fairly large impact on our business. One of these is how consumers pay for their pond installations. When we started our pond business in the mid ‘90s, I would meet a water feature customer at their site, design the pond of their dreams and then provide them with a quote. If the customer wanted to move forward with the project, I would collect a 50-percent deposit and schedule the job.

However, if my quote was more than they could afford to pay, I would offer to make adjustments like taking out the lights or making the pond a little smaller to try to get it within their budget. Sometimes we could reach an agreement, but at times, we could not. Of course, when we could not, I would be disappointed and frustrated — and so was my customer!

There Has to Be a Better Way!

Two things came together to pretty much eliminate this problem. One was menu pricing, so to speak. We took several of our most popular pond and pondless waterfall sizes and created a price menu for our customers to browse ahead of time. We have a display garden where customers can walk among each of the different items on the menu and see for themselves exactly what is included with each of our features.

At first I thought, “Who would ever finance a pond?” I knew people financed cars and houses, but ponds? So whenever I heard a potential customer ask that question, I pretty much wrote them off as “tire-kickers” who really couldn’t afford us.

But when the finance questions kept coming, I realized we had to look into it. Where to start, though? We talked to our local bank, but their setup seemed pretty clumsy. About that time, our supplier announced they would be working with a financial institution to offer financing for ponds. We attended a webinar, and we were amazed at how simple the plan was. We filled out the vendor application, and the rest is history.

How Does it Work?

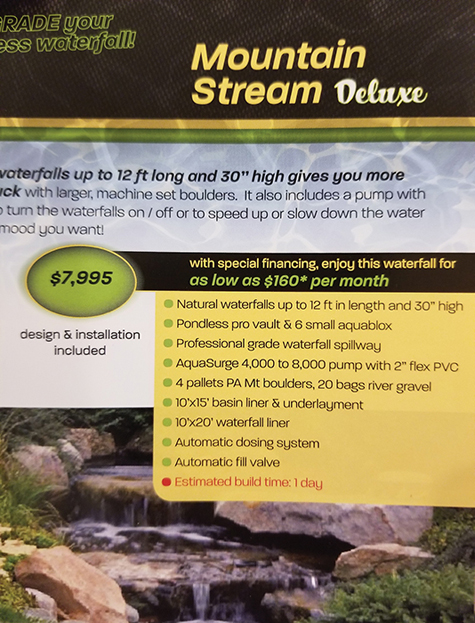

All the items on our pond menu are now clearly labeled with an installation price and the monthly payment amount if a customer chooses to finance the project. (For example, our Serenity Pond installs for $9,625, or $193 per month at a 7.99-percent APR for 61 months.) If they want to finance it, we send them a link to the online application, which takes less than a minute to fill out. Usually within a couple of minutes, they get an email showing they have been approved and how much they have been approved for. We then schedule a site visit.

Site visits are much easier to navigate when both the customer and I know exactly how much they can spend. More often than not, the customer has been approved for more than the cost of the original water feature they chose. This makes it very easy to add things like a longer stream, more lights or even a larger pond. Sometimes the customer comes in thinking they only have the cash for a small pond, and when they see our financing offers, they are quick to choose a larger-sized pond with more options.

One thing I have learned is to avoid trying to figure out if a customer wants to finance. At first, I thought that if a customer drove an expensive car or lived in an affluent neighborhood, they would most likely not need financing.

By the Numbers

When we finance through our institution, we do not collect a deposit before the project begins. We do, however, link the amount for which they are approved to our account, so they can only spend it with our company. As soon as the project is finished, we fax the sales slip to the bank. Payment in full for the entire project is deposited into our account within one or two business days.

The banking institution does, however, charge us, the vendor, 6 percent of each project installed. Right now, we are financing about half of our projects, so we have built 3 percent into all our menu prices to cover this cost and the fee if customers choose to pay with a credit card. The bank also typically charges their vendors a small annual fee, which may be negotiable depending on your institution.

One thing I have learned is to avoid trying to figure out if a customer wants to finance. At first, I thought that if a customer drove an expensive car or lived in an affluent neighborhood, they would most likely not need financing. I now know that the nicer the car or neighborhood, the more likely they are to finance. Even if they can afford to pay for it in full, some banks offer deals like no interest for 18 months, which is a no-brainer for most people. We now include “easy financing available” with all of our advertising, whether on billboards or in social media and mailers.

One thing I have learned is to avoid trying to figure out if a customer wants to finance. At first, I thought that if a customer drove an expensive car or lived in an affluent neighborhood, they would most likely not need financing. I now know that the nicer the car or neighborhood, the more likely they are to finance. Even if they can afford to pay for it in full, some banks offer deals like no interest for 18 months, which is a no-brainer for most people. We now include “easy financing available” with all of our advertising, whether on billboards or in social media and mailers.

Sometimes changes make a big impact for the better. Financing has definitely made a huge impact for us. If you are on the fence about financing, I would encourage you to set it up and then advertise it. I can guarantee that you will be pleasantly surprised with how easy the process is as well as how many customers will take advantage of it.